Why CFOs and Their Tax and Finance Teams Are Playing an Increasingly Strategic Role

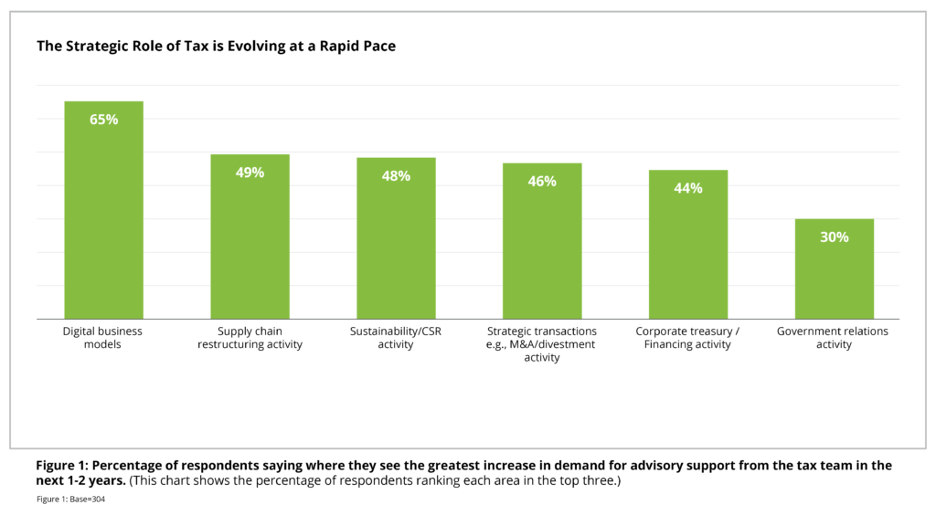

Long before Covid-19, CFOs have grappled with competing priorities driven by traditional responsibilities paired with digital transformation imperatives. Today, the CFO and their tax and finance teams are continuing to play an increasingly critical role in real-time modeling and business structuring. These elevated activities require the ability to unlock capacity to meet both compliance requirements and the strategic demands being placed on the tax function. Tax leaders have become an essential strategic advisor to propose and defend business model changes and supply chain restructuring and to model desired outcomes in response to global economic recovery scenarios.

Now tax teams are being called into action to help their companies navigate new territory, from partnering with HR to assess the impact of displaced workers and remote models, to understanding financial resilience. “The crisis caused a flurry of stress testing exercises which triggered a surge in tax forecasting exercises. We’ve had to do two years’ worth of forecasting in 12 months, so it’s made us take a fresh look at our forecasting processes and how they can become more automated and efficient,” says Richard Craine, Group Tax Director at Barclays.

As stewards of how evolving tax policy will impact business forecasting and profitability—tax leaders will continue to play an increasingly strategic role with the C-suite. Drawing upon a recent survey published by Deloitte, of over 300 tax and finance leaders, this article explores what’s on the horizon for CFOs and their tax and finance leaders.

Tax is Leaving the Tax Department

Some tax and finance leaders see the increased demands of the pandemic as foreshadowing of what is to come. Hybrid product-service offerings, sustainability mandates, digital services taxes, and shifts in compliance reporting protocols resulting from the digitization of tax administrations and real-time reporting requirements are emerging trends that will necessitate strategic guidance from the tax department. To meet the increased demands, CFOs and tax and finance leaders are taking actions now to create additional capacity and control costs.

Rethinking Tax Resourcing Models

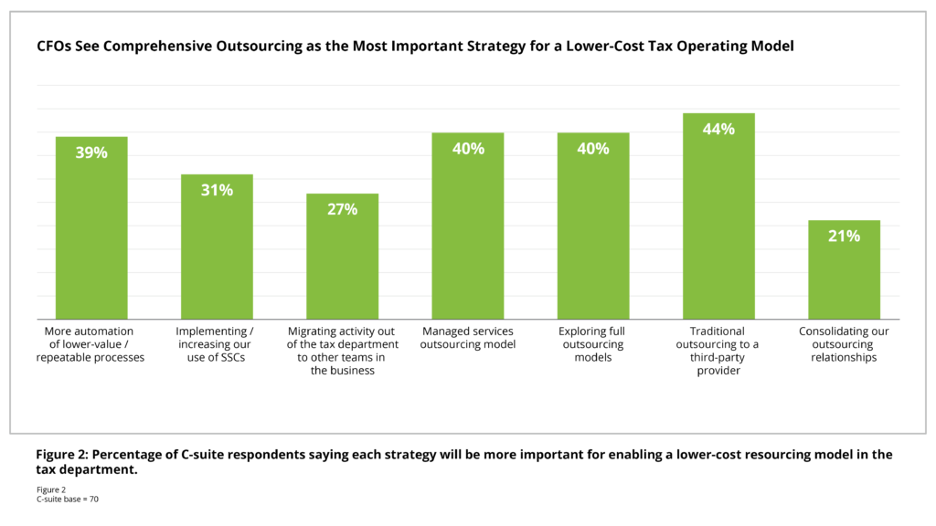

Demands for the corporate tax department to partner with the business are on the rise, but 93% of tax leaders say their department’s budget is flat or falling. To cope and control costs, C-suite leaders, most of whom were CFOs in this survey, are choosing to move increasing amounts of compliance and reporting work to traditional outsourcing providers (44%), managed services or full outsourcing providers (40%), and increasing automation (39%). The survey shows a gap between the strategies the C-suite see as most important (outsourcing) and those Tax leaders see as most important (shifting work to other parts of the business).

Tipping Point

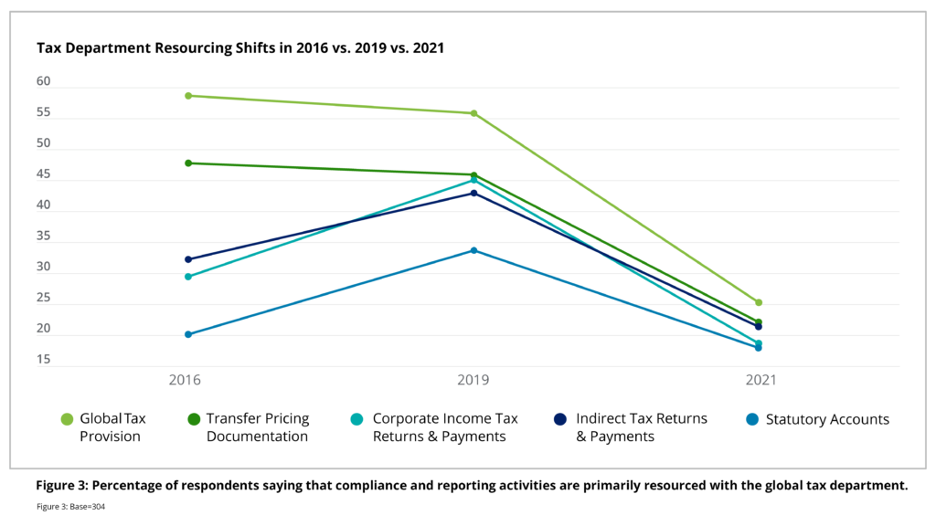

Historical trend data shows a dramatic move of compliance work out of group tax teams between 2019 and 2021, as resourcing models hit a tipping point.

Should tax continue to be primarily a compliance function or is there more to be gained? Tax leaders understand the complex implications of adopting new digital product and distribution models, tax credits, grants, and incentives, and the impact of government sustainability policies. CFOs need to be assessing where the tax department can add the most strategic value to the business and what options are available to increase capabilities and capacity without increasing costs to enable this to happen.

Read the full Deloitte Tax Transformation Trends Survey: Operations in Focus at: https://www.deloitte.com/taxopssurvey

IFRS 17: ‘Beyond compliance’

The new insurance accounting standard (IFRS 17) will transform not just financial statements, but also other aspects of the business including systems.

IFRS 17, mandatory for the period beginning on or after 1 January 2023, represents an opportunity for insurance companies to relook and improve on their systems, processes and data capabilities towards full-scale modernisation.

It is also an opportunity for management to identify opportunities to transform their finance, risk and actuarial processes.

For many insurance companies in East Africa, the new accounting standard is seen as a ‘big deal’ requiring integrated cross-functional approaches towards implementation. They are not wrong; the standard was designed to be principles-based which leads to some challenges in its interpretation and its application in practical terms.

The new standard will require insurers to take a different approach to measuring and reporting insurance and reinsurance assets and liabilities using more granular data, assumptions and models with current supportable inputs.

Designed to achieve the goal of consistent, principles-based accounting for insurance contracts, the new standard requires insurance liabilities to be measured at a current fulfilment value and provides a uniform measurement and presentation approach for all insurance contracts.

New actuarial modelling for IFRS 17 will be required to determine the best and most appropriate estimate cash flows, risk adjustment approach and contractual service margin. Under IFRS 17, an insurer will be required to re-measure its estimates each reporting period using the current assumptions, which will necessitate significant effort and new processes and controls in actuary, risk and accounting.

The standard will also change the way that the insurance industry will report its numbers. At a fundamental level, the way that profits are calculated and monitored over time will change.

The contractual service margin (CSM) represents the future profit embedded in insurance contracts and is almost certainly going to be one of the key performance indicators for insurance companies, among other indicators. It also represents a significant change in how insurers need to think about managing their profit through time. Fully understanding the new measurement of profit, and what drives it, is important.

The new standard will impact many departments and functions across organisations including product design, pricing, actuary and finance. Understanding how to comply and choosing the design of systems and processes will be challenging during the implementation phase of the standard. Significant practical challenges around data, systems and processes are to be expected.

This new standard connects two worlds within insurance organisations that until now have had limited interactions: the actuarial and accounting departments. IFRS 17 will force accountants and actuaries to work and align processes more closely to ensure users of financial statements get the information that they need.

Without question, data is the most important and challenging aspect of IFRS 17 implementation. IFRS 17 has been judged to be a ‘data hungry’ standard; the standard is complex and demanding in both the quantity and granularity of the data required. The most immediate impact of the standard for some companies is that they find themselves lacking the right amount and necessary quality of data needed to implement IFRS 17.

For companies that have the requisite data, the challenge then becomes one of putting in place the required processes and systems to align with the new accounting requirements.

Given the far-reaching impact of the new standard, entities need to put in place clear implementation plans to ensure that its potential impact on the various areas of the business is considered well in advance and where necessary, communication is made to the relevant stakeholders.

Insurers should not underestimate the resources that will be required to implement the required changes effectively and to meet the deadline. Even if the results are targeted for financial reporting, the scope of change goes way beyond what the CFO’s office can undertake on its own.